[ad_1]

I saw the news about the new FHFA lending fee structure for Freddie Mac and Fannie Mae and thought, as usual, things were being blown out of proportion. Then I saw the table for the new fees and I could not believe how they have made it more expensive for high-down-payment borrowers than low-down-payment borrowers. I don’t mean the fees decreased for low down payment mortgages and are closer, but still lower than high down payment mortgages. The total LLPA fees are lower across the board for those who put 5% down or less than those who put 20 percent down.

What are FHFA and LLPA Fees?

LLPA stands for loan level pricing adjustment. They are fees that were put in place after the 2008 crash to help Freddie and Fannie Mae stay solvent during another downturn. The Fees are applied on most conventional mortgages and were set high for low down payment and low credit borrowers because those borrowers are more likely to default. If the fees are higher the banks will typically raise the interest rate on those loans. In the past, people with high credit and high down payments paid lower fees and had lower interest rates.

FHFA is the Federal Housing Finance Administration. FHFA announced that they changed the fee structure in April and has received a ton of backsplash after many sources claimed mortgages for high credit and high down payment borrowers would be more expensive than mortgages for low credit and low down payment borrowers. This is not exactly true in all cases, but it is true that the interest rate will be higher for some people with higher credit and higher down payments than those with lower credit and down payments.

Why did FHFA change the fee structure?

FHFA said:

“It had been many years since a comprehensive review of the Enterprises’ pricing framework was conducted. FHFA launched such a review in 2021. The objectives were to maintain support for purchase borrowers limited by income or wealth, ensure a level playing field for large and small lenders, foster capital accumulation at the Enterprises, and achieve commercially viable returns on capital over time.”

There have been other articles that have claimed race inequality was part of the reasons for the change, but the just of it is, they wanted to make it cheaper for low-income and low-credit score borrowers to buy houses.

FHFA officials have justified this move by saying:

“An FHFA official told The Post the agency was “tasked with ensuring [Fannie and Freddie] fulfill their role in any market condition,” adding that shifts in long-term mortgage rates are a far bigger factor in determining finance conditions in the US housing market.

The latest recalibration to the pricing framework that FHFA announced in January 2023 is minimal, by comparison, and maintains market stability,” the FHFA official said in a statement.”

This is from a New York Post article: https://nypost.com/2023/04/16/how-the-us-is-subsidizing-high-risk-homebuyers-at-the-cost-of-those-with-good-credit/

What they said was that interest rates went up a ton, so you shouldn’t worry about what we are doing. Worry about interest rates instead.

How much more will good credit buyers pay for a mortgage?

While some buyers getting a mortgage will pay less than before, overall the fees will be higher now. The people paying the highest fees will be those with high down payments and low credit. That’s right. I said high down payments. Some high down payment borrowers with good credit will now pay a .2 to .3% higher interest rate than they paid before. In fact, those high down payment borrowers are paying higher fees than those putting less money down! While high credit, low down payment borrowers, may be paying lower fees than before.

On a $400,000 mortgage, a borrower with good credit putting 20% down may pay $40 more a month because of the higher rates. That is not a huge amount but it is tough to bear with interest rates already 2 to 3 times higher than 18 months ago.

How much less will bad credit buyers pay for a mortgage?

Those with lower credit and a high down payment will be paying less than before, but those with low credit and a low down payment get the biggest discount. Some of the worst buyers will now get a .4% discount on their interest rate compared to what they are paying now. Those low-credit borrowers won’t be paying less than high-credit, high-down-payment borrowers, but the gap shrunk significantly.

For someone with a 620 credit score and 5% down or less, they will now save about $80 to $100 off their mortgage payment thanks to the interest rate decrease.

All buyers will now pay more LLPA fees for 20% down vs 5% down or less

The crazy part of these changes is that across the board for good credit or bad credit, all buyers will be paying less LLPA fees for having a lower down payment (unless they put more than 25% down). Someone with an 800 credit score will pay three times the fees when putting 20% down versus putting 5% down or less. Even someone with a 620 credit score will pay less LLPA fees when putting less than 5% down verse 20% down.

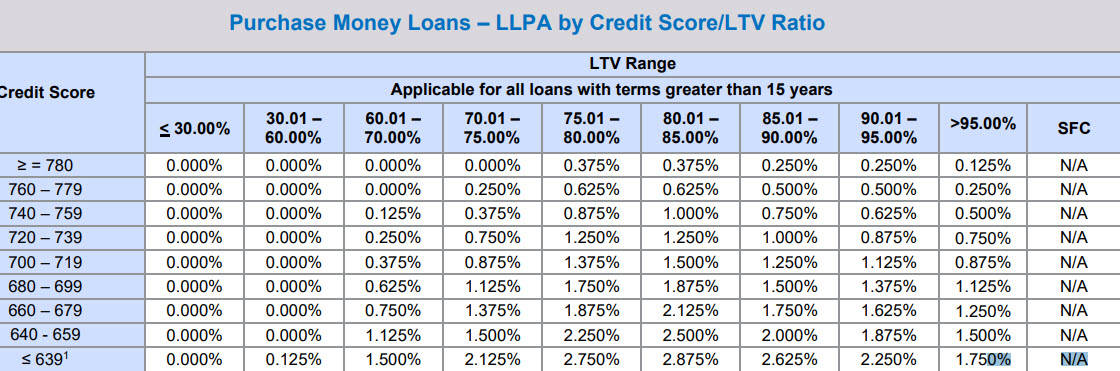

Below is the table showing the new fees:

This is from: https://singlefamily.fanniemae.com/media/9391/display

The left side of the table shows the credit scores and the top shows the loan-to-value ratio (the higher the number the less money people are putting down). There are also many other factors that will impact these fees like debt-to-income ratios, type of property, refinance vs new purchase, etc. The video below goes over the changes in detail.

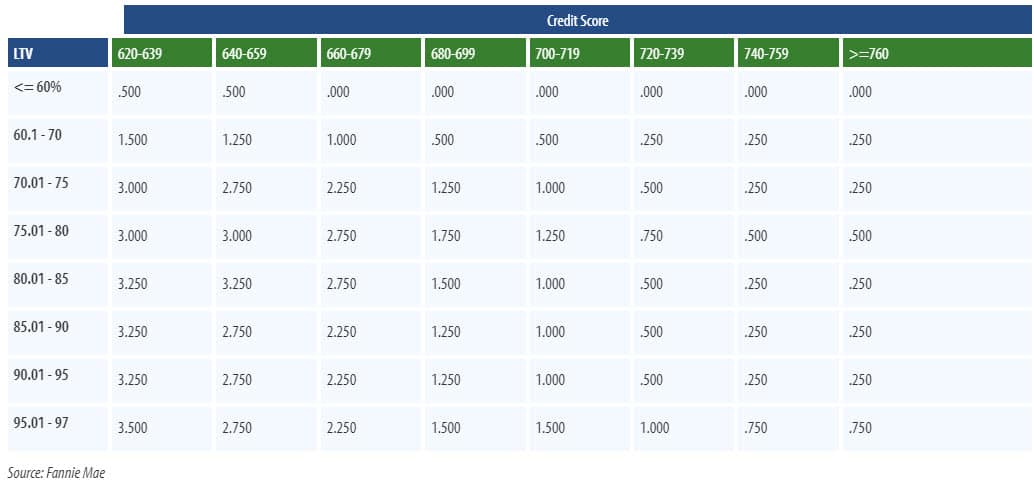

Were the FHFA LLPA fees always structured to reward low-down payments?

I am always skeptical of headlines and crazy stories like this. Many of you probably think it has always been this way, but the old fees were structured much differently. You can see them below:

This chart is from 2020 and can be found at: https://www.freeandclear.com/guides/mortgage-topics/loan-level-price-adjustments.html

As you can see, the fees were higher for low down payments and lower for high down payments. The fees were also higher for lower credit and low down payments. I think common sense tells us this is what the chart should look like.

Do high down payment borrowers really pay more?

FHFA said in a statement that while the fees from FHFA for high down payments are higher than the low down payments, that does not mean those high down payment borrowers will pay more. If you put less than 20% down on a mortgage you most likely will be paying mortgage insurance which would be higher than the LLPA fees. So those who put more than 20% down, will still most likely pay fewer fees. Those who put 15% or 10% down, will still have mortgage insurance and have higher fees and mortgage insurance than those putting 5% or less down.

What the spokesman for FHFA did not mention is that you can often get mortgage insurance removed after a couple of years on conventional mortgages. After the mortgage insurance is removed, many buyers who put less down would be paying a lower rate without mortgage insurance than those who put 20% down.

What is one of the craziest scenarios with LLPA fees?

The Mortgage Interest Rate Is now lower for someone with a 680 credit score putting 3% down than for someone with a 730 credit score putting 15% down. If you look at the chart from FHFA, a person with a 730 credit score putting 15% down would have a 1.25% LLPA fee, and the person with a 680 credit score with 3% down would pay a 1.125% fee. Both of those buyers would pay mortgage insurance.

Conclusion

I could not believe the numbers when I saw them on the LLPA fee table. The media was not overblowing what had happened, in fact, I think they missed how bad it was. These guidelines do not apply to FHA, VA, or USDA but for Freddie Mac and Fannie Mae. Most people with good credit and debt-to-income ratios will be using Fanie Mae and Freddie Mac and are being punished for putting more money down.

[ad_2]

Source link