[ad_1]

The rise of active listings in this spring housing market reminds me of a zombie slowly rising from its grave. Yes, we found the seasonal bottom for housing inventory on April 14, but this year’s rise in active listings has been tepid at best.

Here’s a quick rundown of the last week:

- Total active listings grew 662 weekly, and new listing data is still trending at all-time lows.

- Mortgage rates fell last week as we started the week at 6.65% and got as low as 6.49% to end the week at 6.55%.

- Purchase application data rose 5% weekly as the streak of lower rates impacting the weekly data continues.

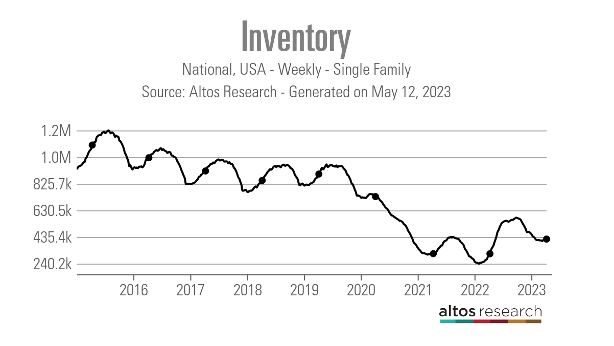

Weekly housing inventory

Well, the best thing I can say for spring 2023 inventory is that we found the seasonal bottom a few weeks ago. On the positive side, we’re at least seeing inventory rise — some had feared that because new listing data was trending at all-time lows, we wouldn’t see a spring increase in the active listings at all. This doesn’t appear to be the case for 2023.

However, new listing data is very seasonal and we have less than two months left before it starts declining again. I had hoped we would see more active listings before that period, but unfortunately that’s not the case. In fact, this data line has been absolutely crazy.

How crazy?

Last year, from April 22 to April 29, total single-family inventory grew by 16,311 in that one week. This year, from the seasonal bottom on April 14 to now — a whole month — total active inventory has only grown by 14,913.

- Weekly inventory change (May 5-12): Inventory rose from 419,725 to 420,381

- Same week last year (May 6-13): Inventory rose from 300,481 to 312,857

- The inventory bottom for 2022 was 240,194

- The peak for 2023 so far is 472,680

- For context, active listings for this week in 2015 were 1,108,932

According to Altos Research, new listing data rose weekly but is still trending at all-time lows this year. When you consider that a home seller is a natural homebuyer as well, you can see why the housing market broke after mortgage rates went on a roller coaster last year. Mortgage rates went above 6.25%, then declined back to 5% then spiked back to 7.37%. We have not been able to recover from that mortgage rate spike and it has bled into 2023 as well.

Last year, new listing data, while trending at all-time lows, was at least rising year over year. That is no longer the case after the second half of 2022.

New listing weekly data for this week in May over the past three years:

- 2023: 62,382

- 2022: 73,515

- 2021: 71,191

New listing data from previous years for the same week, to give you some historical perspective:

- 2017: 90,112

- 2016: 82,621

- 2015: 98,436

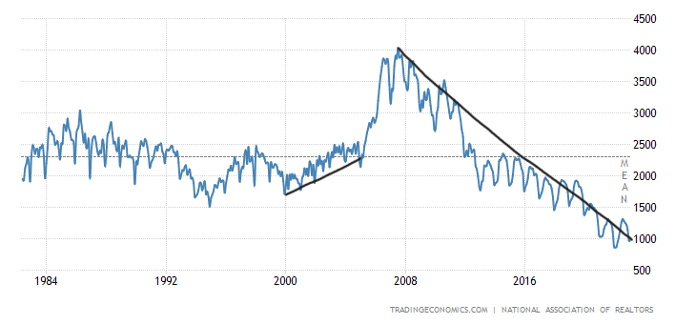

The NAR data goes back decades and it illustrates just how hard it’s been to get the total active listings back to the historical range of 2 million to 2.5 million. The next existing home sales report comes out this week and we should see an increase in active listings, which have been stuck at 980,000 active listings over the last three months.

NAR: Monthly active listings

NAR: Total active listing data going back to 1982

I often get asked about the big difference between NAR and Altos Research inventory data. This link explains the difference. Overall, inventory data tends to move together, even if different sources are working with other numbers and have a different methodology.

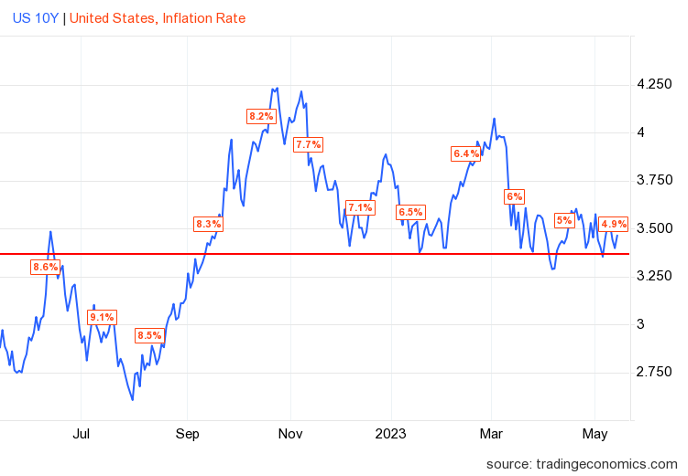

The 10-year yield and mortgage rates

For 2023, one of the most important economic storylines has been the 10-year yield refusing to break below the critical levels I have talked about for months — the level between 3.37%-3.42%. I believed this level was going to be so hard to break under that I named it the Gandalf line in the sand. No matter how crazy things have gotten in 2023, the 10-year yield only broke it once, at the height of the banking crisis. That didn’t last long as we headed right back higher.

As you can see in the chart below, that line in the sand has been tested many times.

When I talk about mortgage rates, it’s really about where I feel the 10-year yield will go for the year. In my 2023 forecast, I said that if the economy stays firm, the 10-year yield range should be between 3.21% and 4.25%, equating to 5.75% to 7.25% mortgage rates.

Now if the economy gets weaker, meaning the labor market sees a noticeable rise in jobless claims, then the 10-year yield should break under 3.21%, going all the way to 2.72%. This will take mortgage rates under 6%, and if the spreads return to normal, this can get us below 5% mortgage rates again. Yes, I said below 5% again.

Can you imagine the housing market at that point? We would have much more stability.

However, for that to happen, jobless claims would need to rise to 323,000 on the four-week moving average. We did have a big jump in jobless claims last week. However, this data line can have some odd quirks week to week, so focus more on the trend and the four-week moving average rather than one week’s data.

From the St. Louis Fed: “Initial claims for unemployment insurance benefits increased by 22,000 in the week ended May 6, to 264,000. The four-week moving average also rose to 245,250.”

Last week, mortgage rates didn’t move much, but as the year goes on, we will be tracking more and more economic data to get clues on the economic cycle and where mortgage rates will be heading.

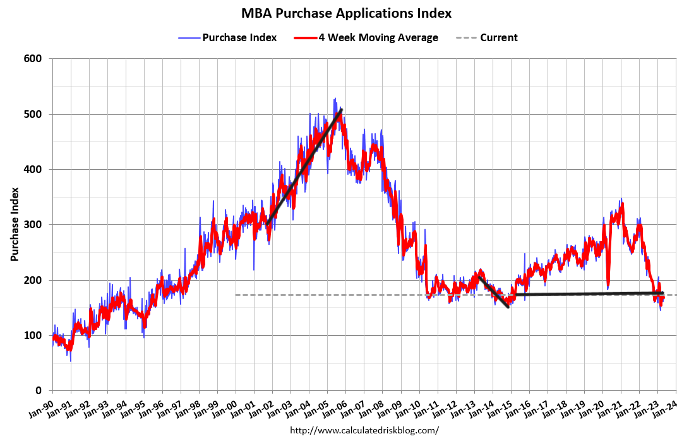

Purchase application data

The dynamics of the U.S. housing market changed starting Nov. 9, 2022, when the purchase application data began to react more positively as mortgage rates fell. Since that time, making some holiday adjustments to the data, we have had 17 positive weekly prints versus seven negative prints. Year to date, we have had 10 positive prints versus seven negative prints.

Last week, the weekly data showed a positive 5% print, while the year-over-year data shows a 32% year-over-year decline.

I view this data line as just a stabilization of the housing demand data, coming off a waterfall dive in 2022. However, this stabilization is critical because of what it has done: It has changed the housing dynamics.

When housing demand collapsed last year, the low inventory didn’t provide a big shield against pricing getting much weaker. Pricing in the second half of the year was going negative month to month, of course, from an overheating start in 2022. Starting from Nov. 9, the entire housing dynamics changed from demand collapsing to demand stabilizing.

This explains pricing getting firmer in 2023 due to the low inventory environment. Purchase apps look out 30-90 days before they hit the sales data, so we don’t have the sharp recovery data we saw during the COVID-19 recovery. However, we do have a good stabilization story here today.

I traditionally weigh this data line after the second week of January to the first week of May, and now that we are in the second week of May, I would say the 2023 purchase apps data is slightly positive, with stabilization for sure, just not a booming mortgage demand market with mortgage rates still over 6%.

The week ahead: Big housing data coming up

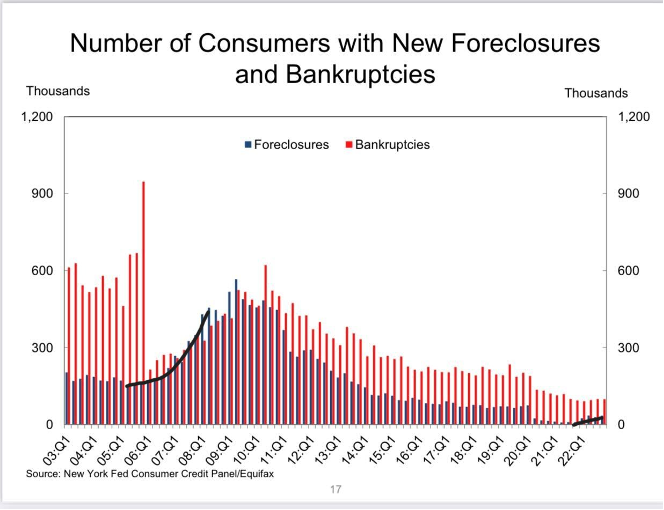

We have a jam-packed week with economic data, especially for housing. We have the builder’s confidence data, housing starts and existing home sales. Monday, we also have the New York Fed quarterly credit and debt update. Those charts are my favorites as they show how credit stress in the U.S. today doesn’t look like anything we saw in the run-up in 2008.

Since the foreclosure process has started again, we should be working our way back up to pre-COVID-19 levels. However, 30, 60, and 90-day lates are near all-time lows, and it took many years to build up the credit stress we saw from 2005 to 2008, before the job-loss recession.

Retail sales come out on Tuesday, which can move the bond market depending on what the report shows. As the year progresses, all these reports will give us more clues to see where the economy is heading. That’s critical since economic data can move the bond market and what can move the 10-year lower or higher drives mortgage rates as well. If mortgage rates head lower, we could see inventory drawn down faster during the seasonal decline period of fall and winter.

[ad_2]

Source link