[ad_1]

Just when I thought it was safe to say we were getting more traditional spring housing inventory , we hit a snag last week, as active inventory and new listings declined. Hopefully, this is just a blip, which can occur from time to time with weekly data. We had a lot of drama over the week between Federal Reserve meetings and banking stress, and mortgage rates and purchase applications both fell.

Here’s a quick rundown of the last week:

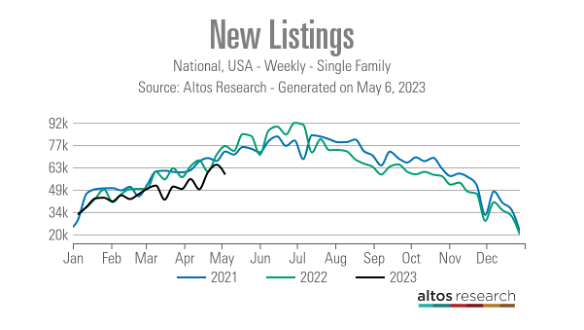

- Total active listings fell by 2,545, and new listing data also fell week to week, continuing the streak of the lowest new listing data ever recorded in history.

- Mortgage rates fell last week as we started the week at 6.73%, got as low as 6.43% to end the week at 6.5%.

- Purchase application data fell 2% weekly as the streak of higher rates impacting the weekly data continues.

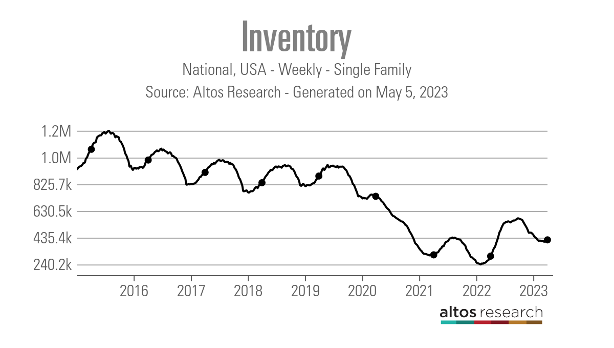

Weekly housing inventory

The numbers this week are unfortunate: inventory should be growing like it does at this time every year. But, the weekly inventory data can occasionally have big moves up or down that can deviate from the longer seasonal trend so I need to see a few more weeks of inventory declining before I make too much out of one week.

However, one thing is for sure, housing is not going to crash due to large-scale panic-selling — a scare tactic of late 2021 that didn’t work then or now. New listing data was trending at all-time lows in 2021 abd 2022 and now it’s creating a new all-time low trend in 2023.

- Weekly inventory change (April 28-May 5): Inventory fell from 422,270 to 419,725

- Same week last year (April 29-May 6): Inventory rose from 287,821 to 300,481

- The bottom for 2022 was 240,194

- The peak for 2023 so far is 472,680

- For context, active listings for this week in 2015 were 1,081,085

Weekly housing inventory

According to Altos Research, new listing data declined weekly and is still trending at all-time lows in 2023. This data line can have some wild swings up and down, but for the most part, we do see the traditional seasonal increase in new listings data. We are roughly two months away from the seasonal decline in new listings.

Since the second half of 2022, after the big spike in mortgage rates, this data line hasn’t gotten much traction. Last year at this time, we saw some growth year over year, but this year it’s been different.

New listing weekly data over the past three years:

- 2023: 58,432

- 2022: 76,691

- 2021: 73,291

New listing data from previous years to give you some historical perspective.

- 2017 99,880

- 2016 88,105

- 2015 94,101

As you can see in the chart below, new listing data is very seasonal; we don’t have much time to get some more growth here.

The NAR data going back decades shows how difficult it has been to get back to anything normal on the active listing side since 2020. In 2007, when sales were down big, total active listings peaked at over 4 million. We had high inventory levels while the unemployment rate was still excellent in 2007.

This proves that the mass supply growth we saw from 2005-2007 was due to credit stress, not because the economy was in a recession; the U.S. didn’t go into recession until 2008. Even though the labor market is currently showing signs of getting softer, there is no job-loss recession yet.

The total NAR inventory is still 980,000. As you can see in the chart below, there is a big difference between the current housing market and those looking for a repeat of 2008.

NAR total active listing data going back to 1982

People often ask me why there is such a difference between the NAR data versus the Altos Research inventory data. This link explains the difference and is worth a read.

While this was a disappointing week on the inventory growth side, I hope this is just a one-week blip. We can see what a difference a year makes in inventory data. For example, last year, from April 22-29, weekly active listings grew by 16,311. So far this year, after the seasonal bottom in inventory happened the week of April 14, the total growth in active listings since that week has been only 14,257.

Traditionally, we would see active listings starting to grow at the end of January. However, that growth has taken longer in 2023 than any other year in U.S. history and so far the active listing growth from April to May has been mild.

The 10-year yield and mortgage rates

Last week we had multiple land mines for the 10-year yield and mortgage rates to rise or fall with the Fed meeting and four labor market reports. Although the Fed raised the Federal funds rate, the bond market is sensing a slower labor market and mortgage rates fell.

Tracking the 10-year yield and mortgage rates are essential for housing inventory because when rates fall, buyer demand gets better, allowing more homes to be bought and getting a lid on inventory growth, which we have seen since 2012. The only two years we have seen the active inventory grow were 2014 and 2022 when softness in demand allowed inventory to grow.

The big difference between 2022 and 2014, as you can see in the chart below, is that the bottom in 2022 was an all-time record low; we can see year-over-year growth in total active listings. However, the increase in inventory this year from last still puts active listings near all-time lows.

NAR Total Active Listings

We have seen from 2022 that the monthly supply of NAR data has grown more visually in the data lines; this means homes are taking longer to sell than before. I wrote about this last week and talked about it in the HousingWire Daily podcast.

NAR Monthly Supply Data

Mortgage rates started last week at 6.73% and fell as the labor data and banking stress drove money to the bond market. We briefly broke under my key Gandalf line in the sand (between 3.37%-3.42%) intraday, only to close right at the line and rise by the end of the week. This line has been truly epic.

Mortgage rates fell to a low of 6.43% then ended the week at 6.5%. The spreads between the 10-year yield and 30-year mortgage rates have been terrible for a long time and have gotten worse during the banking stress. While credit is stlll flowing for conventional loans, mortgage pricing has been bad. Mortgage rates in a regular market should be 5.25% today but are at 6.5%. Can you imagine the housing market at 5.25% today when we found stabilization with rates ranging between 5.99%-7.10% this year?

In my 2023 forecast, I said that if the economy stays firm, the 10-year yield range should be between 3.21% and 4.25%, equating to 5.75% to 7.25% mortgage rates. If the economy gets weaker and we see a noticeable rise in jobless claims, the 10-year yield should go as low as 2.73%, translating to 5.25% mortgage rates.

Of course, the banking crisis has added a new variable to economics this year. However, even with that, the labor market, while getting softer, hasn’t broken yet. We have been in the forecasted range all year, even with all the drama from the banking crisis, which isn’t good news for the economy.

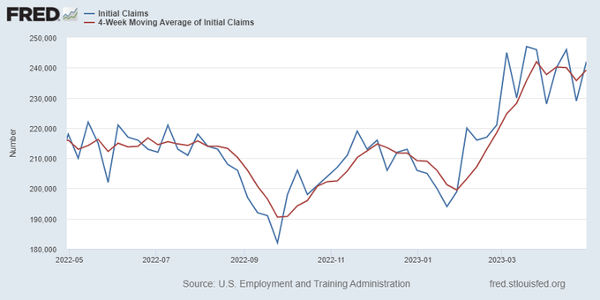

My line in the sand for the Fed pivot has always been 323,000 jobless claims on the four-week moving average. This has been my big economic data line for the cycle since I raised my sixth and final recession red flag on Aug. 5, 2022. While the labor market is getting less tight, it’s not broken yet.

From the Department of Labor: Initial claims for unemployment insurance benefits increased by 13,000 in the week ended April 29, to 242,000. The four-week moving average also rose by 3,500 to 239,250.

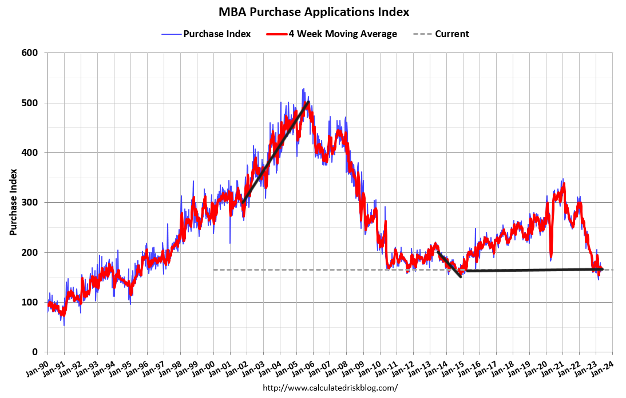

Purchase application data

Purchase application data has been the main stabilizing data line for the housing since Nov. 9, 2022, with 16 positive prints versus seven negative prints, after making some holiday adjustments. For 2023, we have had nine positive prints versus seven negative prints.

The MBA purchase application data line has been very rate-sensitive: when the 10-year yield and mortgage rates rise, it typically produces a negative weekly print, and when they both fall, we get a positive print. This past week we saw a 2% week-to-week decline in the data line.

The year-over-year decline in purchase application data was 32%; as I have noted, we are working from the mother of the all-time lowest bars in 2023. As we can see in the chart above, just having 16 positive prints since Nov. 9 has stabilized the data — it’s been hard to break lower than the levels we saw back in 1996.

The year-over-year comps will get noticeably easier as the year progresses, especially in the second half. This data line looks out 30-90 days for sales, and we are almost done with the seasonality. I always weigh this report from the second week of January to the first week of May. Next week for the tracker, I will report on how 2023 demand looks based on this index.

Traditionally, purchase application volumes always fall after May. Now, post-COVID-19, this index has had some abnormal late-in-year growth data. So, after May, I will address this issue with seasonality and whether we will see some growth later in the year, as we have seen in previous years.

The week ahead: It’s Inflation week!

All eyes are on the CPI report this week, coming on Wednesday, and we have the PPI inflation report on Thursday. The entire market knows the headline inflation growth rate peaked last year, so watch out for the core inflation data, excluding shelter inflation. Of course, core CPI is primarily driven by shelter inflation, and we all know by now that it will cool off, especially as the year progresses. However, the Fed and the markets focus on service inflation, excluding shelter.

I am keeping an eye on the car inflation data as that might be stubborn this week, keeping core inflation higher than it should be.

The bond market never bought into the 1970s inflation premise, so the 10-year yield is closer to 3% than 5%. Since the entire marketplace is keeping an eye out on credit getting tighter, I will be watching the Senior Loan Officer Opinion Survey on Bank Lending Practices on Monday. This will provide more clues into how fast credit is getting tighter in the U.S. economy, which is key at this expansion stage.

So, we will have some economic data to see if the 10-year yield can break lower and send mortgage rates lower as well. So far, the Gandalf line in the sand has held up against some brutal attacks this year, but we shall see if we can break under that line of 3.37% and head lower in yields. Why is that important? Because the 10-year yield and mortgage rates have always danced together, and if the 10-year yield heads lower, mortgage rates will follow it.

[ad_2]

Source link