[ad_1]

Is the labor market finally normalizing? Jobs Friday data came in as a beat of estimates, but the labor market is clearly starting to come back to earth, killing the fear of 1970s wage spiral inflation. We’ve had a good week’s worth of data to show that the Federal Reserve is starting to get what it wants if you know where to look.

The headline jobs data beat estimates, but we did have 149,000 negative revisions to the previous month’s data. However, the cumulative labor data this week is a story of job growth returning back to normal and the Fed should be happy because the labor market has always been its target for pain.

From BLS: Total nonfarm payroll employment rose by 253,000 in April, and the unemployment rate changed little at 3.4 percent, the U.S. Bureau of Labor Statistics reported today. Employment continued to trend up in professional and business services, health care, leisure and hospitality, and social assistance.

Part of my COVID-19 recovery model on the labor market was that job opening should reach 10 million in this recovery. The Federal Reserve was terrified of this because this could send wages spiraling out of control, which means they had to kill this labor market. Nothing is worse to the Fed members than 1970s inflation.

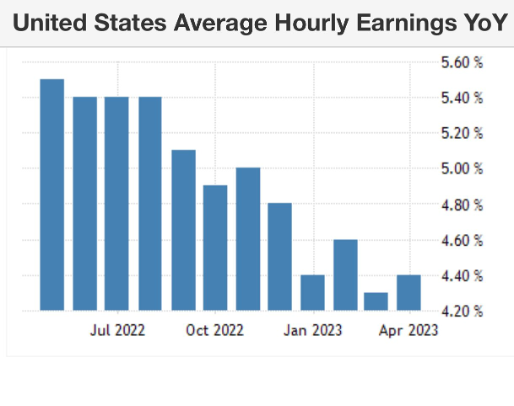

That isn’t happening today. As we can see, wage growth has been cooling down, even with a tight labor market. Yes, wage growth has slowly decreased while millions of jobs were being created and we had massive job openings.

Even if we added other variables, such as hours worked, we could see the wage growth data cooling.

Also, this week we learned that the one data line Fed cares about, job openings, are no longer at 12 million. That number is down roughly 2.5 million since 2022. The Fed wants this to return to 7 million to feel more comfortable about the labor market. The reason I say 7 million is because that’s where we were before COVID-19 happened.

Job openings data

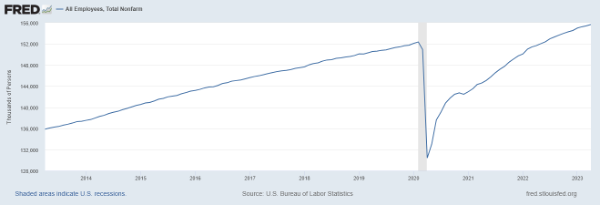

One thing to remember about this labor market and the historically low unemployment rate of 3.4% is If we didn’t have COVID-19, total employment in America would be 158 million to 159 million, just taking the pre-COVID-19 growth trends.

Based on demographics, I wasn’t a huge job creation person in the previous expansion. However, the shock of Covid created a significant fall in employment, and while it has been spectacular to see the rise of people being hired again, we are still in make-up mode as long as demand is growing.

If we didn’t have COVID-19, the total number of jobs would be higher today, but the job growth numbers would be lower. So, if some people are surprised about the job data at this cycle stage with all the rate hikes and bank drama, don’t forget this reality when considering the job growth we have seen since 2022.

Total employment data: 155,673,000

Now let’s look at the internal report for more details.

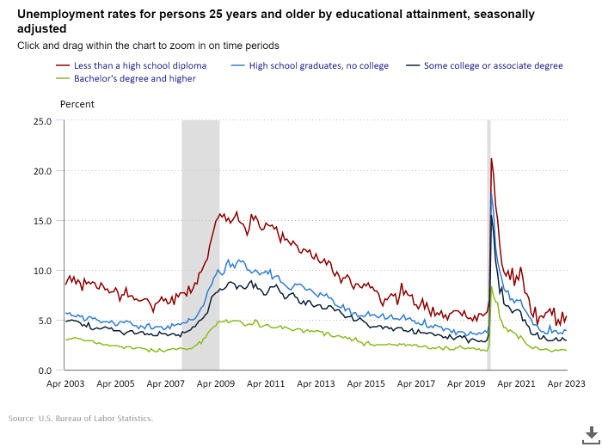

One of the data lines I have stressed during the past decade is the unemployment rate tied to educational background. This is useful for housing data, especially when the next recession hits. Here is a breakdown of that data for those aged 25 and older:

- Less than a high school diploma: 5.4% (previously 4.8%)

- High school graduate and no college: 3.9%

- Some college or associate degree: 2.9%

- Bachelor’s degree or higher: 1.9%

Yes, you saw right, college-educated Americans with a Bachelor’s degree have an unemployment rate below 2%, which means they’re in great demand.

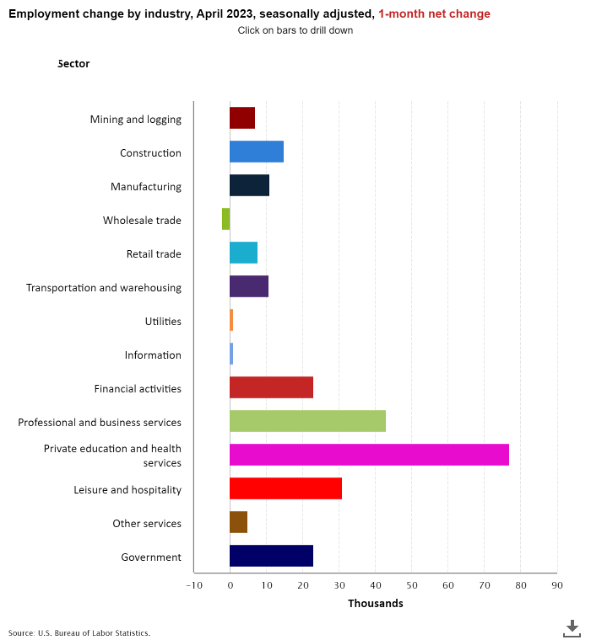

This report shows the sectors where the jobs were gained and lost. Most sectors this month had job gains, of course. But, if we take a three-month average of job gains in the private sector only, not accounting for the government, it’s running at 182,000 per month, the slowest pace of job growth since early 2021. Again, the Fed is getting what it wants, the labor market to cool off.

My 2023 forecast for the 10-year yield and mortgage rates was based on the economic data remaining firm, meaning that as long as jobless claims don’t get to 323,000, we should be in a range between 3.21%-4.25%, with mortgage rates between 5.75%-7.25%. Right now, jobless claims are at 242,000.

If the labor market breaks, the 10-year yield could reach 2.73%, which means mortgage rates could go lower, even down to 5.25% — the lowest end of my range for 2023.

Even though we had a lot of drama this week in the market, my famous Gandalf line in the sand for the 10-year yield didn’t break. I’ve said for many months that this line is a tough nut to crack and on Friday afternoon before close the 10-year yield was around the 3.37%-3.42% level, as the chart below shows.

Overall, April was a good jobs report; nothing is wrong with the labor data now in a meaningful way, but we see that the growth of job creation is slowing down, which was always going to be the case coming back from the depths of COVID-19.

When does the labor market break, meaning jobless claims data shoot up much higher? Even though job openings data has noticeably come down, we haven’t seen jobless claims data spike out of control, which is the most critical data line we have with labor.

I joke that in the rock, paper, scissors game, jobless claims beat job openings always. The Fed knows that all their rate hikes have a lag before they hit the economy. We can clearly see that the fear of wage growth spiraling out of control is not happening and that, over time, the inflation growth rate will ease.

What’s next?

Over the next 12 months, we will see more of an impact from the massive rate hikes and credit getting tighter from the banks, this is why it’s more critical than ever to track weekly economic and housing data, as we do in the Housing Market Tracker every week. Like every economic cycle post-WWII, if you know where to look for clues, they will guide you to the truth.

[ad_2]

Source link